Industry leaders size up prospects and challenges in the year’s final CPE 100 Sentiment Survey.

At the end of a tumultuous year, the views of commercial real estate executives about the industry’s near-term prospects and challenges appear to be shifting noticeably, the CPE 100 Quarterly Sentiment Survey indicates.

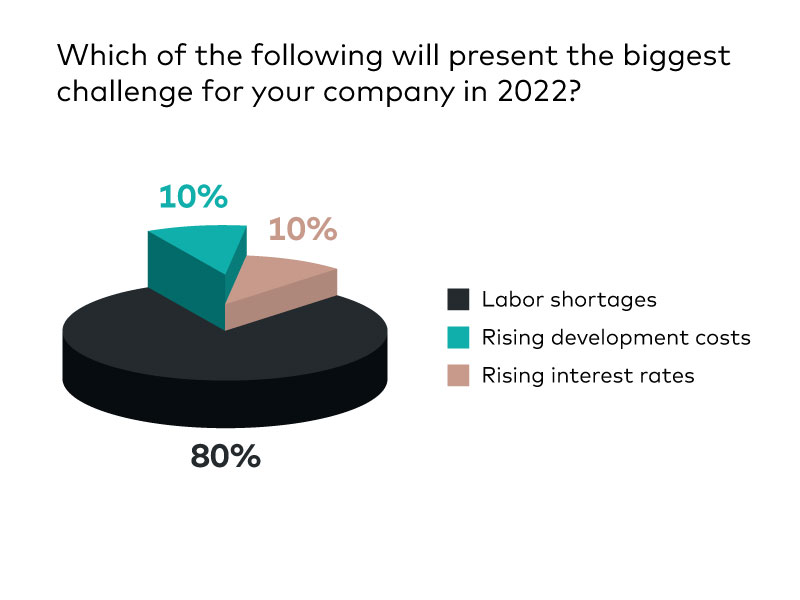

Perhaps the most dramatic change is in the CPE 100’s views of the challenges immediately ahead. A large majority of respondents—80 percent—cite the labor crunch as the likely No. 1 issue for next year, according to the survey of industry leaders. During the fourth quarter of 2020, the issue most often mentioned was reduced opportunities for revenue, named by 42 percent.

In another notable turnaround, 70 percent of executives expect investment activity in 2022 to be about the same as in 2021. That reflects a big change from one year ago, when 75 percent of those surveyed said that there would be somewhat more deals in the year ahead.

The recent emergence of the omicron variant may have dampened earlier expectations for the near future. For the first three quarters of the year, the share of the CPE 100 which believe that general business conditions will get better over the next six months has hovered consistently between 50 and 60 percent.

But in the second half, CPE 100 members looking to the next six months have been increasingly likely to say instead that business conditions will be unchanged. Thirty percent of respondents now hold that view, according to the latest survey.

From the third to fourth quarter, the percentage expecting business conditions to get at least somewhat better has slipped from 58 percent to 40 percent. And in a departure from the preceding three surveys, 20 percent of survey participants now think that business conditions will be worse in six months.

Suggesting a perception that the economic recovery is beginning to level off, Sentiment Survey participants have become more circumspect about the prospects for their own firms’ performance. As recently as the second quarter, 94 percent of the CPE 100 predicted that their companies would be doing somewhat better or much better six months in the future.

By contrast, just half of survey respondents now expect improvement in six months. The share who say that their companies will be doing about the same has jumped from just 6 percent during the second quarter to 50 percent now.

CBRE is maintaining a positive outlook for the economy and commercial real estate in 2022, despite uncertainty over potential impacts of the COVID omicron variant and other risks. While the new variant will impact the timing of a large-scale return to the office, fiscal and monetary policy remains highly supportive of economic growth. There may be other bumps along the way, notably from the ripple effects of an economic slowdown in China and rising oil prices, but the factors that held back growth in 2021—labor shortages, supply disruptions, inflation and other COVID variants—will ease. Monetary policy will tighten to keep longer-term inflation pressures in check, which may trigger some short-run volatility in the stock market, but it will not be enough to dampen investor demand for real estate.

We foresee a record year for commercial real estate investment, enabled by high levels of low-cost debt availability and new players drawn to real estate debt’s attractive risk-adjusted returns. Commercial real estate values will rise, particularly for sought-after industrial and multifamily assets. Investors will sharpen their focus on emerging opportunities in the office and retail sectors in search of better returns.

The supply/demand balance in the office sector will remain highly favorable for occupiers, but the pace of recovery will pick up following a sluggish 2021. With hybrid work the new normal, office properties with amenities that enhance employee collaboration, connection and wellness will fare best.

Retail, by contrast, is seeing the effects of a longer-term transition, which has included pricing adjustments, low levels of new construction and beneficial investment in the best experiential and convenience-led centers. Sales-to-square footage ratios are surging and the demographic- and pandemic-induced shift to the suburbs will favor grocery-anchored and neighborhood centers. With strong forward returns now achievable, we anticipate a decade-high level of retail investment volume in 2022.

Industrial & logistics hardly broke step during the pandemic as e-commerce surged. 2022 will see slower demand for physical goods as the service sector reopens and attracts more consumer spending. This will give supply a chance to catch up with demand. Third-party logistics operators are beginning to dominate the sector and are looking to get ever closer to the end consumer.

Multifamily will continue its recovery in 2022, with downtown locations returning to pre-pandemic occupancy levels. Single-family rentals in the suburbs will also fare well as some millennials leave the city to raise families.

A notable trend in the second half of 2022 will be the return of downtowns. As business and tourist travel picks up, we will see a sharp revival in the hotel sector in gateway cities, alongside the already recovering food & beverage sector. This, in turn, will stimulate the return to the office and the fuller recovery of downtown life.

The outlook for real estate in 2022 is positive, with big cities potentially surprising on the upside. Amid this recovery, ESG, demographics, digitization and decarbonization will take on a new importance.

We have produced this report to help you navigate the macro environment we expect in 2022 and look forward to working with you in the new year.

The outlook for real estate in 2022 is positive, with big cities potentially surprising on the upside.

Multifamily

The multifamily sector is set for a record-breaking 2022 amid solid fundamentals and heightened investor interest. With tremendous liquidity and a growing range of debt options available, multifamily pricing will be as strong as ever.

Record-high demand and construction pipeline

The U.S. multifamily sector is poised to finish 2021 with overall occupancy and net effective rents above pre-pandemic levels. While certain markets face challenges, the overall health of the sector will lead to a record 2022.

The growing economy is boosting household formation, which had been artificially suppressed by the pandemic. New households are catalyzing demand for rentals, which is expected to match the pace of new deliveries in 2022. We forecast multifamily occupancy levels to remain above 95% for the foreseeable future and nearly 7% growth in net effective rents next year.

Construction will remain elevated in the near term. Completions in 2021 will likely reach a new high, and another 300,000-plus units will be delivered in 2022. For context, deliveries averaged 206,000 units annually since 2010 and 171,000 per year since 1994.

Despite strong demand, the volume of new Class A product coming online will limit the performance of higher-quality assets. However, Class A rents were most negatively affected during the crisis and there is more room to recover. Overall, we project 8% growth in urban effective rents in 2022. These exceptional growth rates will moderate to 3% in 2023 and slightly below that in subsequent years. These strong fundamentals, together with the expectation that debt will remain available and at a relatively low cost, is welcome news to developers as construction costs rise.

From urban to suburban—and back again

Downtown multifamily properties are filling back up and occupancy rates are nearing pre-pandemic levels, spurred by a confluence of factors: fewer restrictions on urban amenities, higher vaccination rates, a growing willingness to use public transit, the reopening of college campuses and more workers returning to the office.

Urban areas saw an average vacancy rate increase of nearly 200 bps during the peak of the pandemic. As of Q3 2021, urban vacancy rates average 5%, just 70 bps above their pre-crisis level, and are expected to fall to 4% by the end of 2022. By contrast, suburban properties fared better, as both secular and cyclical factors—income uncertainty, a preference for outdoor options, a need for more space and more millennials with growing families requiring schools—drove demand for apartments in lower-density and lower-cost submarkets.

Figure 1: Urban Vacancies Expected to Fully Recover in 2022; Suburban Vacancy Remains Stable

As of Q3 2021, urban vacancy rates average 5%, just 70 bps above their pre-crisis level, and are expected to fall to 4% by the end of 2022.

Investors still favor multifamily

We predict U.S. multifamily investment volume will reach a record of nearly $213 billion in 2021 (year-to-date volume totaled $179 billion through Q3 2021), well above 2019’s level of $193 billion. For 2022, we expect at least a 10% increase from 2021 to $234 billion.

While capital continues to flow from both domestic and foreign sources, the targets seem to be shifting. Investors find strong non-coastal markets more acceptable than ever and there is also a growing trend toward favoring ESG compliant assets, especially from European investors.

The Federal Housing Finance Agency (FHFA) established a $78 billion cap on multifamily purchase volumes for Fannie Mae and Freddie Mac for 2022, up 11.4% from 2021. This level of liquidity should facilitate strong value growth. In addition, we expect a resurgence in the flow of foreign capital targeting multifamily assets. Liquid multifamily debt capital markets, which includes traditional lending sources and alternative lenders like debt funds and mortgage REITs, will further stabilize and could even compress cap rates—even as interest rates rise.

Investment strategies for 2022

As always, multifamily investment strategy relies on a balance between risk and reward. Class A assets in urban areas—particularly in gateway cities—present tremendous opportunities. These markets were hit hard during the pandemic-led downturn but have the most favorable outlook over the near and medium term. However, they also present some downside risk amid new domestic migration patterns.

Lower-risk, lower-reward markets include strong secondary ones that were less affected by the pandemic. Markets like Atlanta, Dallas, Denver and Philadelphia are expected to offer more modest income and appreciation returns compared with gateway markets and a relatively stable investment return outlook.

Markets with increased regulation—particularly those with new or proposed rent controls—limit the income opportunities from rent growth and require greater operational efficiency to drive NOI.

Figure 2: Multifamily investment to set new records in 2021 and 2022

Trends to watch

The rise of single-family rentals The single-family rental market will gain traction with both renters and investors as more millennials reach child-rearing life stages. Urban apartment operators will rely more on Gen Z to backfill the resulting vacancies.

Return to the office will spur urban demand Rising office occupancy will boost urban multifamily demand. We project that U.S. office workers will spend an average of 3.4 days per week in the office going forward, down a full day from the 4.4-per-week average in 2018. While living near the office may not be as important in the future, it will remain a key consideration for many renters.

Employment Market Firms Amid Wane in Infections; Winter Headwinds Present

Job creation picks back up. After a slowdown in August and September, hiring improved in October as 531,000 personnel were added to staffs. A downshift in the number of coronavirus infections and the expiration of federal unemployment benefits likely contributed to the greater job creation. Employment growth was most prevalent in the leisure and hospitality sector, predominantly at bars and restaurants, as well as in professional and business services. Last month’s gains helped lower the unemployment rate 20 basis points to 4.6 percent, above the 3.5 percent pre-pandemic low but below the long-run average.

Industrial sector posts landmark performance.Amid an ongoing labor shortage, the transportation and warehousing sector added an above-average 54,000 positions last month, reflecting the current state of supply chains. Production delays and port congestion have prompted some retailers and online marketers to increase inventories, adding to warehouse space demand, while the upcoming holidays portend an uptick in distribution volume. Hiring by manufacturers also climbed to 60,000 personnel in October, suggesting these firms are now receiving or are about to collect the parts they need to resume production. Last month’s employment figures signal industrial space demand continues to increase after a record 157 million square feet was absorbed in the third quarter, lowering vacancy to an equally notable 4.4 percent.

Foot traffic at retailers and hotels improves. Bars, restaurants and other retailers expanded headcounts by 154,000 last month, a positive sign that fewer COVID-19 cases translated into greater visits to stores. Nationally, retail vacancy fell 20 basis points year over year in September to 5.3 percent, the first annual decline since 2018. Asking rents also modestly improved, up 2.5 percent on average. Lower health risk may have also prompted more people to travel last month, when 23,000 new positions at hotels were added. Hotel occupancy averaged close to 63 percent in October, up 30 percentage points from a year prior. While occupancy is set to decline through year-end, the driver is traditional seasonality.

Additional Trends

Declining teleworking benefiting office space demand. In October, only 11.6 percent of the employment base worked remotely because of the health crisis, down significantly from 35.4 percent in May 2020. While more employees could possibly be teleworking now for other reasons, the health-related barriers to office returns are declining, affecting space needs. More office space was leased than vacated in the third quarter, the first time this has happened since the first quarter of 2020. These trends suggest that as a sector, office properties may be turning the corner.

Increasing COVID-19 infections raise concerns for winter. After cresting in September, the delta variant wave abated in October, aiding hiring. Coronavirus case counts began to trend up late in the month, however. Going forward colder weather will push more people indoors, increasing infection risks, although broader immunity will likely keep infections from climbing as high as last winter. More companies implementing vaccine mandates may also hinder future job growth, with impacts varying by geography and industry.

Kansas City is experiencing exceptional annual rent growth and positive net migration which is fueling aggressive out-of-state buyers to enter the Kansas City multifamily market. With more capital than ever targeting the Midwest, price per unit sales and average cap rates have reached all-time record levels.

Historical Sales & Rent Growth in Kansas City

Kansas City By the numbers

Supply, Demand & Rent Growth

Surging effective rent growth is projected to peak in 2022 before returning to the historical average. Supply is expected to outpace demand over the next several years.