Panelists of the discussion include, from left: Mike Eckert, Daniel Brocato, Sheryl Vickers, Yianni Vrentas and DeJ’on Slaughter. Kelli Keedy moderated this portion of the event.

Kansas City has seen a deluge of exciting real estate development over the past few years. Now, local real estate professionals are challenged with multiplying that good fortune, panelists said at the second annual Kansas City Forecast Summit.

The panel took place at the Medallion Theatre at the Midtown Plexpod location and was hosted by Midwest RE news.

Panelists covered topics such as multifamily development, adaptive reuse efforts, the state of the local real estate market, regional economic development opportunities and game-changing projects.

Here are three takeaways:

Adaptive reuse renaissance

Adaptive reuse can be scary because of the risks that come with it. MR Capital Advisors President Bob Mayer said project leaders must embrace the risks that come with those projects, especially when there’s a historic layer to a development.

“Sites that are adaptive are often blighted, and the crappier the project, the better the opportunities are,” Mayer said. “Public/private partnerships are the only way to make these deals work.”

The $118 million, 11,500-seat Kansas City Current stadium will break ground in October. This rendering shows what it will look like when it’s finished. GENERATOR STUDIO

Racking up wins

The nearly finished Kansas City International Airport terminal and announcement of a dedicated stadium for the Kansas City Current are two major achievements for Kansas City. Now, developers must spread the wealth to other areas in the city, panelists said.

Panelists talked about how to add infill development to the Prospect area, change offices to suit a post-pandemic world and invest in industrial space.

CBRE Senior Vice President Matt Eckert said office tenants want to align with the “workplace of tomorrow,” which might mean moving to a nicer building in areas like the College Boulevard submarket.

Select Sites LLC CEO Sheryl Vickers said developers must seek out incentives or create incentives to attract retail tenants. This can be done by pushing for tenant improvement money or developing on the outskirts of popular retail districts.

“If you know what everyone needs, from transit platforms to the city to residents, et cetera, and align them all, projects will be successful, and they will go where they make sense,” Vickers said.

Work continues on the streetcar’s southern extension. This image shows construction workers aligning two sections of rail before they are welded together. ADAM VOGLER I KCBJ

Looking ahead

Real estate professionals should be on the lookout for the next popular area for development.

Kansas Streetcar Authority Executive Director Tom Gerend said that once the $350 million southern extension is complete along Main Street from Union Station to the University of Missouri-Kansas City, Kansas City must look east to west and by the river to extend it even farther.

“Ten years from now, we’ll have an operational spine on Main Street, and we’re actively looking at the next round of expansion, specifically looking east to west and north of the river to grow the city as sustainably as possible,” Gerend said. “It’s never just been about the streetcar, but more-so how we can use our platform to help facilitate the needs each corridor and neighborhood.”

More development on the East Side and the West Bottoms may be on the horizon, Mayer said. It depends how long investors and developers are willing to hold a building or property.

Panelists also considered their vision for the future of the industry. They talked about uplifting underrepresented colleagues and finding solutions for affordable housing.

“We need minorities owning and developing their own neighborhoods, which means training, mentoring, giving opportunities to women and minorities in your corporations and companies,” Vickers said.

Block & Co. Inc. Realtors Vice President Daniel Brocato said affordable housing should include single-family homes, not just multifamily rentals.

“Houses aren’t going for $80,000 anymore,” Brocato said. “They’re going for $253,000, which is not attainable for a lot of younger families. Owning a home is the greatest way for young people to build wealth for themselves and for future generations.”

Job Growth Downshifts to Goldilocks Zone, Providing Runway for Fed to Pull Off Soft Landing

Last month’s employment report ideal for Fed objectives. Employers added 315,000 personnel to payrolls in August, below the 526,000 jobs created in the previous month, but well above historical averages. The month-over-month hiring slowdown, together with a slight increase to unemployment, lowers the likelihood of a 75-basis-point rate hike at the next Federal Reserve meeting in favor of a smaller margin. The central bank is still likely to raise the overnight lending rate at least one more time this year to bring the target range above 3 percent. Comments from Chairman Jerome Powell at Jackson Hole last month indicate the Fed expects to impose some near-term challenges on the labor market as it pushes interest rates higher in an effort to combat elevated inflation.

Medical-related real estate sees improvement. One of the sectors that led hiring last month was healthcare, with employers in these fields growing staff counts by 48,000 personnel, about double the long-run average. Jobs were distributed among medical offices, hospitals and residential care facilities, reflecting the health needs of the population and driving demand for such space. Medical offices have outperformed traditional offices during the health crisis, posting more consistently positive net absorption and stronger rent growth. Seniors housing facilities have also noted strong demand of late. About 48,600 units were absorbed over the year ended in June, double the units relinquished over the preceding period. Occupancy at skilled nursing properties has also gained about a third of the ground lost during the pandemic. Lack of labor remains an impediment to growth, so last month’s hiring is a positive signal.

Domestic manufacturers need space, personnel. Staff counts among manufacturers continued to trend up last month. More firms are investing in United States operations, especially in fields relating to semiconductor chip, energy storage and electronic vehicle manufacturing. Recent public policies support this trend, creating demand for industrial manufacturing space. On the distribution side of the sector, warehouse demand could wean over the coming year as some retailers re-balance safety inventories.

Labor market entrants nudge up unemployment. The unemployment rate rose 20 basis points in August to 3.7 percent, which is still very low by historical standards. This modest uptick was primarily driven by more people entering or returning to the labor force. The labor force participation rate, which measures the number of people working or looking for a job, increased last month to 62.4 percent, a pandemic high that is nonetheless 100 basis points below the February 2020 mark. Additional available labor should aid firms’ hiring efforts, cooling some upward wage pressure. Lower wage growth would, in turn, help slow inflation.

Total labor force returns to pre-pandemic size. An additional recovery signal, the total civilian labor force grew last month to 164.7 million people, surpassing the 2019 high for the first time. While the number of workers is already at an all-time standing, more people entering or returning to the labor pool to look for work speaks well of the potential capacity of the labor market to meet companies’ personnel needs in the coming months.

The U.S. single-family for-sale market may be at an inflection point given increases in mortgage rates that are likely resulting in supply ebbs, but the Single-Family Rental and Built-For-Rent (SFR and BTR) sector keeps going from strength to strength in both rent growth and investor demand. A pioneer in BTR and SFR investment sales, Berkadia recently issued a white paper, “A Closer Look at the U.S. Single-Family Rental Market,” looking at yields, rent growth and interest rate sensitivity, among other topics. “While BTR and SFR communities have enjoyed strong demand for many years, work-from-home trends spurred by the global pandemic, are contributing to a renter population finding single-family rentals more attractive than ever,” the white paper states.

Phoenix-based Mark Forrester, senior managing director for investment sales, and director Andrew Curtis sat down with Connect CRE recently to provide their take on the current market. The team has completed numerous BTR/SFR transactions in several Smile States of the U.S. and Phoenix, and like most Sun Belt markets, has registered strong upside deviation–i.e. rental growth rates above their historical averages—as studied in the white paper.

The white paper shows a strong correlation between the current interest rate environment and single-family rent growth. Historically, that correlation has sometimes been detrimental to rent growth. That’s certainly not the case today.

During the nine years that Forrester has been in the BTR/SFR space, rent growth has been impressive. It was “strong when inflation was very tame and continues to be strong, in large part because of the demand for this product, compared to the availability,” he told Connect.

“There’s a lot of this product under construction now, but this new inventory is needed, given the existing overall housing shortage. Whenever we sell one of these communities, the communities have leased up quickly with minimal, if any, concessions,” Forrester said. “We’ve normally seen rents increase during the lease-ups, and then after the initial leases are in place, they’re either renewed or replaced by the second or third wave of leases, resulting in significant further net effective rent growth. In short, BTR/SFR has been very well received, whether there’s been an inflationary spike or not.”

Demand is coming both from traditional apartment dwellers, former homeowners, individuals that are either not yet ready or aspiring to home owners, all wanting “the next best thing to a house,” said Forrester. “And that really plays into this market. One BTR developer we often represent, says this type of product is really the alternative to a starter home.”

Simultaneously, “rising interest rates are making it even more difficult for somebody to buy a house,” Forrester said. “So, I think even more people that would love to buy a house are now looking at this product as well.”

“And, of course, the foundation for all of this is the fact that Smile States, like Arizona and Phoenix in particular, are benefiting from the most robust employment and job growth going on anywhere in the country right now,” continued Forrester. “That means migration to the area is outpacing housing supply of either for-sale or for-rent product. As a result, we should see continued rent growth, even while we have rising inflation.”

The white paper makes the point that going back to the late 2000s and the Global Financial Crisis, the markets in the Sun Belt and especially the Southwest saw the fastest rates of recovery as far as single-family rent growth was concerned. “As expected, across all market types there exists a trend where strong SFR performance occurs alongside strong multifamily performance in the same market,” according to the white paper. That dynamic has if anything intensified, given the current state of home prices compared to a decade ago.

“The average house price in Phoenix in 2010, 2011 and 2012 was, at times, under $200,000,” Forrester said. “It’s now approaching $500,000. The price of a house has gone up so much and yet more and more people are coming here.” That’s helping fuel expansion in the SFR sector.

Additionally, he said, “some homeowners would like to live in a house, but simply wish to avoid responsibilities that ownership entails. A fundamental tenet behind BTR /SFR is providing that resident the advantages of owning what is very much like a house from a privacy standpoint, from having a pet standpoint, from having more space and a backyard standpoint, and yet they don’t have the obligations of a house. Property management takes care of all repairs and maintenance. Plus the residents do not have property taxes and a mortgage payment, meaning it’s a much more carefree style of living.”

“A CNBC article recently came out showing mortgage applications down to the lowest level in 22 years,” Curtis said. “More people are being priced out for every uptick in an interest rate, taking homebuyers out of the market, which in turn will continue to put pressure on these single-family communities as they have record occupancy and people wanting that next best thing. The rent growth is just going to continue to climb as there’s low supply interest rates pulling people out of the housing market overall.”

He continued, “We’re calling it the next best thing, but sometimes it’s a more preferred alternative, also because you’ve got the flexibility. You’re not buying a home with a 30-year mortgage; you’re moving into a rental with maybe a six- to 12-month lease. So, you have flexibility down the road to either renew your lease or buy a house. I think it’s a preferred style of single-family living sometimes for people, even if interest rates were not going up.”

As strong as the appeal of SFR is for renters, it’s equally compelling for investors, despite cap rate compression. “The cap rates and the overall yields, generally speaking, are not unlike what they would be for conventional apartments,” said Forrester. “And what we’ve seen lately is that sometimes the yield for single-family for-rent properties is even a little bit lower than conventional buildings, because there’s more and more demand for people coming into the space.”

Private capital was pretty much the sum total of the investor universe for the SFR product when Berkadia began arranging financing and sales in the sector. Today, though, “you’ve got more and more institutional players coming into the space, because they see it as a permanent part of multifamily going forward,” Forrester said.

Forrester and Curtis recently closed on the sale of a new-construction build-for-rent property, “and the buyer was the separate account for a major pension fund advisor.” said Forrester. “That type of client was not there a couple of years ago.” The presence of greater competition sometimes drives down yields a little more, he added.

The yield compression has been ongoing since the GFC, Curtis pointed out. “We had double-digit yields then. And as the home values continue to increase year-over-year, the yields have compressed even further downwards, largely due to the home price appreciation outpacing rent growth at the time.”

Accordingly, investors are emphasizing rent growth and a steady income stream from rental housing as opposed to yields. Forrester said, “People are buying not only because of the going-in cap rate, but because of the anticipated future increases in cash flow coming primarily from rent growth.” Also, the operating expenses on SFR units tend to be a little less than for a conventional apartment.

“You don’t have quite as much staffing,” said Forrester. “Your turnover ratio is lower. These people tend to be stickier. They stay longer. They just move to another apartment building. If somebody moves on one of these properties, they’re likely going to either buy a house or maybe move to a different part of the nation. So, your operating expenses tend to be 5% to 10% less and your revenue is a little bit higher.”

Current conditions in the capital markets may cast some uncertainty over SFR investor demand for the balance of 2022 and into early 2023. “We all know the capital markets are in turmoil. However, interest rates are increasing for BTR and SFR investors and multifamily investments in general,” said Forrester. “Overall multifamily sale prices, in my opinion, have probably plateaued for the time being. On a case-by-case basis, investments sales demand may begin to slip a little bit just because it’s more expensive to finance anything that you buy right now than it was in the past.”

Having said that, though, he added, “I’d like to think it’s proving out, at least so far, that the BTR/SFR segment of multifamily is likely to hold up as best as any part of the multifamily housing space, because of the significant rent growth going on in that sector and the increasing demand from a wider universe of investors to be in this space.”

“It’ll be an interesting second half of the year, as some investors have hit the pause button momentarily, since they don’t quite know what to do, said Forrester. “But, as we get clarity again, you’re going to see an ongoing trend toward investing in multifamily. Overall, I think it’s going to continue to be a favorite asset class. Secondly, I think single-family for-rent will do as well, or better, than other sectors of multifamily.”

Forrester concluded, “The difference compared with 2021 is that near-term investment demand will likely come from investors that are lower leveraged, whether it be institutional or very strong private capital as opposed to higher leveraged investment capital. So, these investors are likely less sensitive to ongoing increases & volatility in interest rates because they’re more focused on long-term appreciation and increases in cash flow coming from rent growth and ongoing operations.”

“My crystal ball is not that great, but I think in at least the near term, multifamily is still going to be a very good place to be,” he continued. “We may just have more variety in the participants owning in this space, compared to what we had over the past two or three years.”

Figure1: Recent transaction: The Carnival Building, 800 Broadway Boulevard, Kansas City, Missouri; Office/Multifamily Conversion; Closed; 40,500 SF

Class A Attracting Majority of Market Activity

Market vacancy in Kansas City increased to 14.4%, up 50 basis points from the prior quarter. The market realized an increase in asking rental rates in the second quarter of 2022, as rents slightly increased to $21.36/SF, up $0.11/SF from the first quarter of 2022. While the overall trend in asking rental rates since the second quarter of 2020 continues to increase, tenants are often seeing more concessions in the form of free rent and tenant improvement allowances to offset the increase, as well as longer lease terms to accommodate the ever-increasing construction costs. As trailing 12-month inflation continues at 40-year record levels, real asking rental rate growth is stagnant across many metro markets in the U.S. Total market net absorption in the quarter measured negative 137,877 square feet, bringing the total for the past four quarters to negative 972,582 square feet.

Construction projects currently underway total 319,492 square feet. The former Waddell & Reed office headquarters, located at 1400 Baltimore Ave. in Downtown, delivered 260,000 square feet of Class A space to the market during the quarter. Market fundamentals for the second half of 2022 will remain contractionary as tenants continue to evaluate ever-changing space needs. New or newly renovated Class A office space in marquee submarkets which combine easy accessibility, and a prime amenities package will remain in demand, even as rental rates increase. Class B space owners with dated space will face an uphill battle attracting prospects and retaining current tenants during the next four quarters. Tenants will continue to maintain considerable leverage for the remainder of the year in most Metro submarkets.

Price Brothers Purchase Lighton Plaza, a Three-Building Office Portfolio for $61.8 Million

South Johnson County continues to lead the market in sales activity as BentallGreenOak divested a three-building portfolio to Price Brothers for $61.8 million, or $130/SF. The transaction is the largest in the market by sales price dating back to the start of the pandemic. Totaling 475,800 square feet, the Class A portfolio included the six-story, Lighton Plaza I located at 7300 College Blvd., the six-story, Lighton Plaza II at 7400 College Blvd. and the 14-story, Lighton Plaza III at 7500 College Blvd.

The portfolio was approximately 81% leased at the time of sale and includes tenants such as Wells Fargo, Foulston Siefkin LLP, Regus, Burns & Wilcox and New York Life Insurance Co.

Academy Bank Moves Corporate Headquarters from Town Pavilion to 1201 Walnut

Academy Bank announced in June it will relocate its corporate headquarters from Town Pavilion to 1201 Walnut, occupying a total of 49,790 square feet. With corporate offices located on the 10th, 11th and 12th floors, Academy Bank’s new space will feature a first-floor banking branch in the lobby, which is expected to open by the fourth quarter of 2022. The relocation will reduce the firm’s footprint by 31.3%, following a trend of recent office space downsizing. Academy Bank is a subsidiary of Dickinson Financial Corporation, a family-owned and locally headquartered financial services holding company.

Asking Rental Rates Are Expected to Range from $21.20/SF to $21.80/SF During Next Four Quarters

The Kansas City office market loosened in the second quarter of 2022 as negative 137,877 square feet were absorbed. With net absorption during the past four quarters totaling negative 971,582 square feet, average quarterly net absorption has significantly decreased, measuring negative 358,201 square feet during the past 10 quarters. Although the market has already begun to adjust to work-from-home and hybrid workplace strategies, expect a decrease in total net absorption to continue to take place during the second half of 2022. Leasing commitments during the quarter were active, especially in the Downtown/Crown Center and South Johnson County submarkets, as tenants locked in favorable terms for new direct and subleased spaces.

Expect favorable conditions and opportunities for prospective tenants to upgrade from Class B to Class A space during the next four quarters, as two submarkets in the Metro display vacancy rates for Class A space exceeding 23% and three additional submarkets display vacancy from 14.3% to 17.9%. Concessions in the form of abated rent and additional tenant improvement allowances, plus inflationary pressures offset by longer lease terms, continue to assist in driving asking rental rates upwards. Overall market vacancy should range from 14.4% to 16.1%, while asking rental rates are expected to range from $21.20/SF to $21.80/SF during the next four quarters.

Economic Conditions

The local economy continued to improve in May, with total employment growth of 1.4% and growth occurring in six out of ten industries, calculated on a 12-month percent change basis.

Payroll employment in Kansas City decreased to 1.4% in May 2022 compared to 7.2% in May 2021. The national average also decreased substantially, down from 9.0% in May 2021 to 4.5% in May 2022.

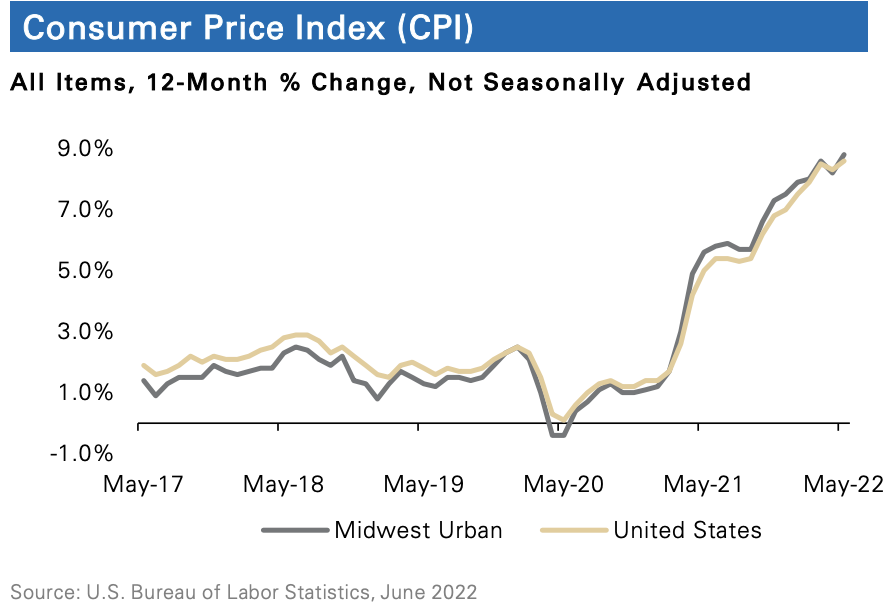

The Consumer Price Index for the U.S. increased 360 basis points compared to the prior year, registering 8.6% in May 2022, while the Midwest Urban CPI increased 320 basis points to 8.8%, both at record highs during the past four decades.

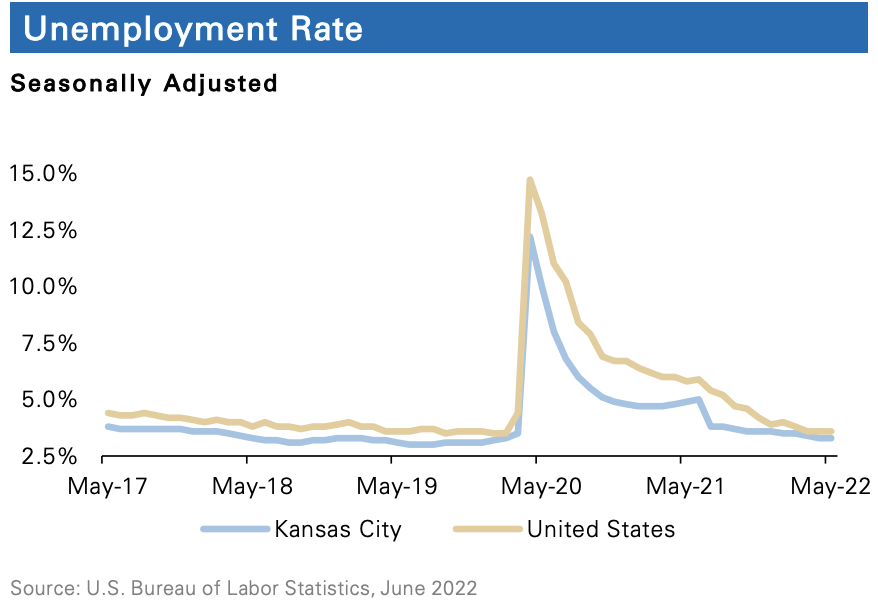

Unemployment in the U.S. decreased 20 basis points to 3.6%, while unemployment in Kansas City decreased 20 basis points to 3.3% compared to the past quarter. Unemployment in Kansas City decreased 160 basis points from a year prior.