Executive Summary

- As concerns over credit availability and a potential recession eventually begin to wane, multifamily is poised to see a significant resurgence in investment activity.

- For the first time since CBRE began polling investors, respondents to CBRE’s Global Investor Intentions Survey in late 2022 said that they would target multifamily properties more than any other property type this year.

- In late 2022, nearly 70% of multifamily investors in the Americas said they expected to keep their allocation to real estate about the same in 2023. Another 20% said they expected it to increase.

- Investors in the Americas had inflation expectations that were more pessimistic than what has transpired in 2023. Most investors expected inflation would peak in 2023 and remain above 4% at year-end. In reality, inflation peaked in mid-2022 and is expected to fall well below 4% in Q4.

For the first time in CBRE’s Global Investor Intentions Survey seven-year history, investors said they were targeting multifamily more than any other property type. Thirty percent of all global investors said that multifamily was their No. 1 target, including 37% of Americas investors. Investors were true to their word, as multifamily has accounted for the largest share of U.S. investment (32%) in H1 2023. However, investment volume across all asset types including multifamily is down significantly this year due to the high cost of capital and macroeconomic uncertainty.

Inflation expectations overblown

Nearly two-thirds of investors predicted inflation would peak in 2023 or later when we conducted the survey in late 2022. However, the Consumer Price Index (CPI) has been steadily falling since peaking at 8.9% in June 2022. It currently stands at 3.7%. CBRE expects annual inflation to end the year at 2.9%, compared with more than half of surveyed investors’ earlier expectations of more than 4%.

Figure 1: CBRE House View

Shelter component of CPI will ensure inflation continues to fall

Expectations that inflation will continue to fall is driven by the CPI’s shelter component. Shelter costs account for the largest portion (43%) of Core CPI, which excludes food and energy prices.

The CPI’s shelter component has two primary metrics: “Owners’ Equivalent Rent of Residences” (this is the amount of rent a homeowner would get for renting out their home at market rates) and “Rent of Primary Residence” (the current cost of rent). Both of these metrics peaked in Q1 2023. Looking at more real-time rent data from CBRE Econometric Advisors, actual rent growth peaked a year earlier in Q1 2022. Given that rent growth has continued to decelerate over the past year, we expect that the CPI’s shelter component will drop over the next 12 to 18 months.

Figure 2: CBRE-Measured Rent Growth vs. CPI-Measured Rent Growth

Source: CBRE Research, CBRE Econometric Advisors, Bureau of Labor Statistics, Q2 2023.

Multifamily investors’ concerns

Investors in our year-end 2022 survey expressed four primary concerns: rising interest rates, credit availability, fear of a recession and persistent inflation. Inflation was a less serious threat by midyear. As for the others:

- The Fed will likely leave interest rates at the current range of 5.25% to 5.50% for the rest of the year. This is higher than initial investor expectations for 2023, as only 8% of survey respondents predicted interest rates of more than 5.0% by year-end. CBRE expects the Federal Reserve to begin slashing interest rates in the first half of 2024 with the fed funds rate ending the year between 4.50% and 4.75%.

- Credit availability remains a legitimate concern. More than 90% of respondents to CBRE’s 2023 U.S. Lender Intentions Survey said their underwriting would be more conservative and 68% expected lower originations in 2023. This is consistent with actual market performance so far this year.

- Near-term recession expectations have become much less certain as the year has progressed. While some economists envision a “soft landing” for the economy, CBRE expects a moderate recession to begin in early 2024 as the lagged impacts of tight monetary policy more fully take hold.

Investor preferences

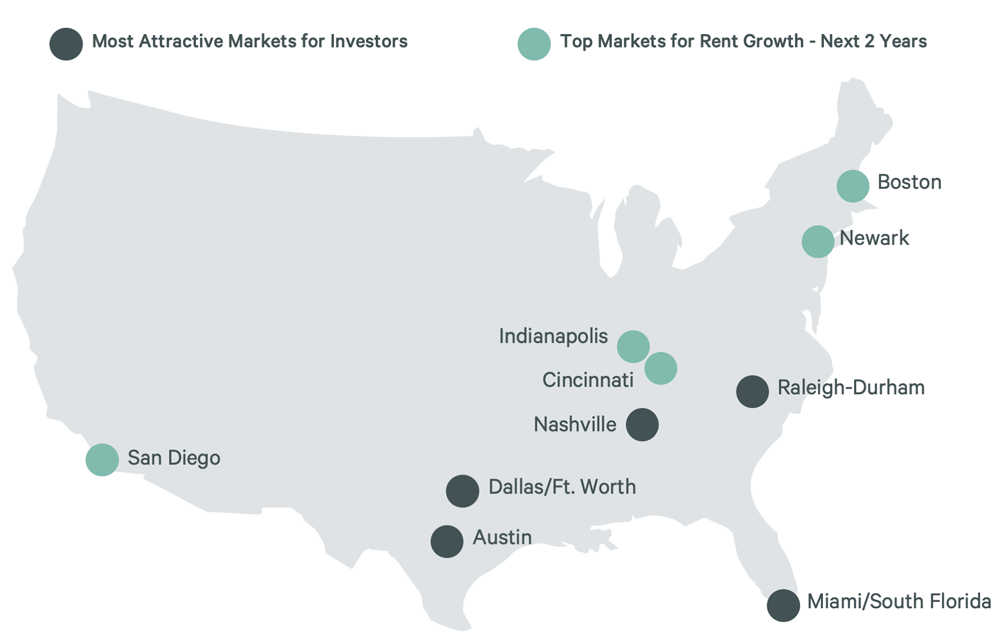

A majority of investors in our survey said they would target certain Sun Belt markets that had the highest rent growth in 2021 and 2022. These are also markets that now have some of the largest pipelines of new supply coming online over the next several quarters, which has suppressed rent growth over the short term. We expect robust rent growth in these markets will resume once supply and demand are better balanced.

As for new opportunities, there are several Midwest and Northeast markets, including Indianapolis and Boston, that provide near-term rent growth potential since they did not have a glut of new construction. These markets offer significant cost savings relative to other areas of the country.

Figure 3: Top investor targets for 2023 vs. top markets for future rent growth

Looking Ahead

Overall economic indicators, including slower job growth, receding inflation and the likelihood that interest rate hikes will now pause, are a mixed bag relative to investors’ initial expectations. However, these indicators generally favor multifamily investment. As inflation and interest rates further stabilize, we expect greater investment activity over the next 18 months. As the favored asset type for investors, multifamily will likely be the first to benefit.

Original and credit: https://www.cbre.com/insights/briefs/midyear-pulse-check-us-multifamily-market